IFRS 18

IFRSs (International Financial Reporting Standards) have been undergoing one of the most significant changes in presentation in the past twenty years, with the new IFRS 18 standard replacing the previous IAS 1 standard.

IFRS 18 will be mandatory for reporting periods beginning on or after 1 January 2027 under the International Financial Reporting Standards (IFRS®),but companies are permitted to apply it earlier.

IFRS 18 – aim of the new reporting structure

IFRS 18 has been developed in response to investors’ serious demand for more comparability in the financial performance of companies.

Users of financial statements prepared in accordance with IFRS® Accounting Standards have voiced concerns that profit or loss and other comprehensive income for the period reported by individual entities may contain significant differences and thus be difficult to compare, due to the different internal structure and content of the financial statements. This difference in the presentation of performance for a given period may make analytical comparisons between companies considerably more difficult.

The new IFRS accounting standard issued by the IASB (IFRS 18) aims to reduce this potential difference in form and content to a certain extent by providing a more structured set of rules.

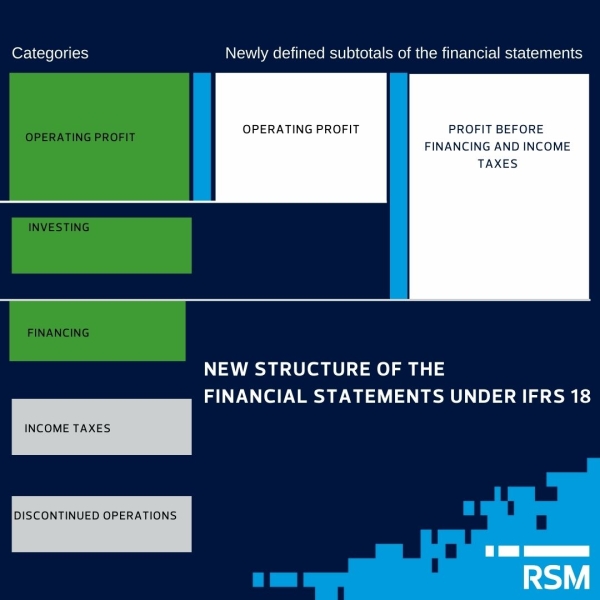

New structure of the financial statements under IFRS 18

IFRS 18 requires the presentation of three new categories in the statement of profit or loss and comprehensive income for the period: operating category, investing category and financing category. It also requires two newly defined and regulated subtotals: operating profit and profit before financing and income taxes.

I. New profit categories

Following the adoption of the new IFRS standard, the statement of profit or loss and other comprehensive income for the period will need to be split into three components. It will therefore be necessary to distinguish between income and expenses classified into the operating, investing and financing categories. In addition, income taxes and discontinued operations will be included in the financial statement.

In defining these three categories, the scope of the entity's activities will be seriously assessed.

The investing category will help the elaborate analysis of income and expenses that arise separately from the enterprise's direct activities.

This category will include income and expenses relating to affiliates and joint ventures, income and expenses relating to cash and cash equivalents, and income and expenses from assets that can be considered as separate from the direct activities of the entity.

Several items need to be classified in the financing category, which will include income and expenses related to bank loans and bonds reported as liabilities, as well as similar items for other liabilities.

The operating category includes all income and expenses that do not fall under either the investing or financing category, and are not part of income taxes or discontinued operations.

In accordance with previous IFRS, the income tax and discontinued operations categories continue to be presented separately in the statement of profit or loss.

The income tax category includes income tax expense or income and related foreign exchange differences arising from income tax expense or income in accordance with IAS 12 Income Taxes.

Income and expenses relating to discontinued operations under IFRS 5 will be classified in the discontinued operations category.

The IASB's research shows that a large proportion of companies have previously reported a subtotal line for operating profit, but they used different methods for calculation, and they were not easily comparable.

The new categories to be presented in the statement of profit or loss and comprehensive income under the new IFRS accounting rules, as detailed above, are intended by the legislators to facilitate comparisons of companies' financial performance and provide a consistent starting point for financial statement analysis.

II. New performance indicators

A new area in the standard is the regularisation of management-defined performance measures, which can be particularly useful to investors in assessing the performance of a company.

IFRS 18 introduces a new requirement to disclose the methodology and additional information in the notes to the financial statements on how the performance measures are determined.

Management-defined performance measures are measures of profit or loss and other comprehensive income that entities use in their public communications outside their financial statements to communicate management's views on certain aspects of financial performance.

These are performance measures that are not included separately in IFRS 18 or in any other IFRS accounting standard. It is therefore appropriate to show how they relate to the indicators set out in IFRS® Accounting Standards.

IFRS 18 focuses on the structured disclosure of information, and the requirements of the standard are designed to improve the clarity of reporting.

Overall, IFRS 18 represents a major change in the presentation of financial statements. The newly defined structural and disclosure requirements may prompt companies to review and prepare well in advance of the effective date.